Published: 19/02/2024 By Claire Matthews

As we approach the end of the tax year, turpin barker armstrong are focused on making sure that our clients are not only making use of their tax allowances and exemptions for the year but also helping to maximise investment returns.The past year or so has been interesting as for once in a long while we have seen better rates of investment return from cash ISA (Individual Savings Accounts) than stocks and share ISAs. This has led to many locking away some of their savings into fixed rates for 12 months to benefit from a tax free 5% return. However, interest rates are predicted to fall this year and so it is highly likely that the days of these higher interest rates are numbered. In fact, we have already seen interest rates being reduced for savers in recent months.

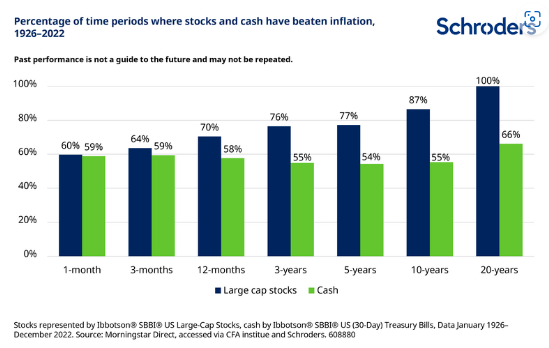

In contrast to the predicted reductions in interest rates, most investment managers are predicting exciting times for investment markets in the coming months. A reduction in interest rates should see a natural increase in equity markets as businesses show a return to better profitability which in turn should see rising stock markets. Statistics have shown that large company stocks have outperformed cash returns consistently. – source Schroder article by Duncan Lamont CFA, 21st August 2023.

Could now be the time to consider making use of your £20,000 ISA allowance for the current tax year?

It may also be the time to consider transferring those cash ISAs that are coming off of their fixed rates and onto lower rates, into a stocks and shares ISA to benefit from the expected growth over the medium to long term.

Don’t forget that parents and grandparents can also contribute up to £9,000 into a Junior ISA on someone else’s behalf.

Should you wish to receive advice on your ISAs, please do not hesitate to contact us. We offer whole of market independent advice tailored to your needs.