Published: 06/02/2025 By Oliver O'Brien

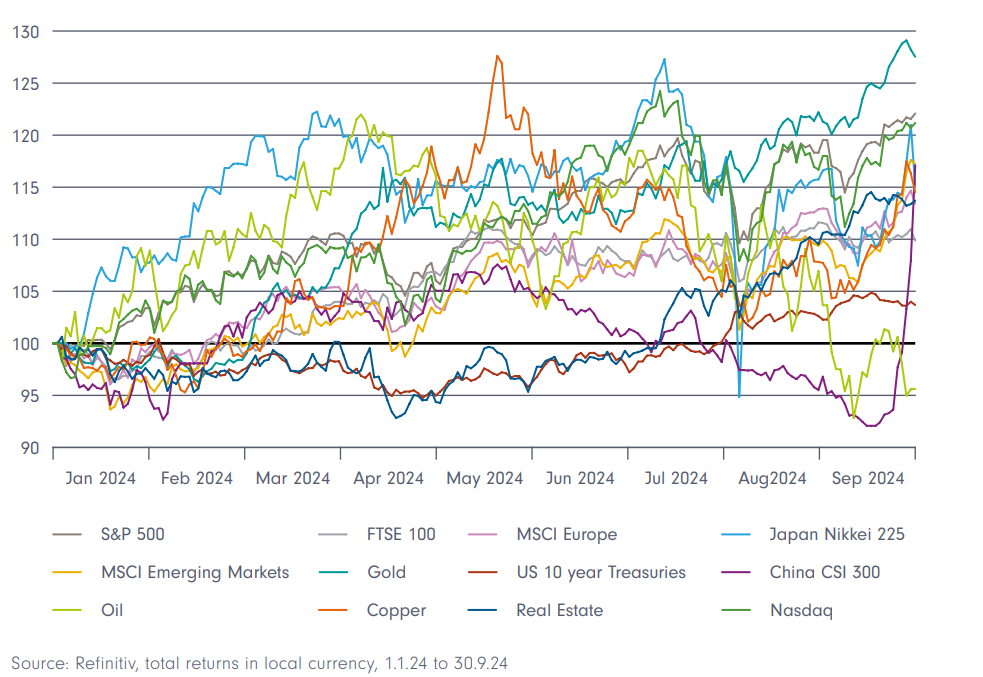

2024 in ReviewFor equity investors, 2024 was a surprisingly good year. Markets had a strong 8 month run and despite a lull in late summer, hit record highs in the last quarter of the year. Traditional economic indicators proved unreliable as economies showed unexpected resilience and growth, rather than expected contraction and recession. A large part due, once again, to strong US large cap (market capitalisation, meaning the total value of a publicly traded company so companies like Amazon, Apple etc) performance and a boom in AI leading to big tech stocks surging once more.

However, significant unpredictability remains. With the continued defiance to many historically proven economic assumptions, this serves to only further emphasise how diversifying your investment portfolios is critical for successful long-term investors.

US Equity

The S&P had a bumper year, closing at 25%. Ultra-cap tech stocks continue to dominate, fuelled by a boom in AI related optimism. This continued strength in US markets continued despite the Fed maintaining interest rates in anticipation of any potential inflationary pressures induced by the new, incoming administration.

The uncertainty lead to combinations such as prospects of market deregulation bumping up value stocks to 12.3% while gold, a “flight to safety” commodity, closed out at 27.1%.

UK Equity

Sluggish in comparison to the US but beating out Europe with equity returns of 9.1%, UK markets have broadly recovered from its 2022 lows despite repeated assaults by the UK media trying to present dismal expectations. Initial optimism from a new Labour government was dampened by a budget that promised larger tax rises than anticipated. The impact of these tax rises will need careful consideration as 2025 progresses.

European Equity

Similarly to the UK, European markets lacked the raw momentum of the US. Their manufacturing sector was hit hard by high energy costs, new regulation and a lack of export demand from the US and China. Limited exposure to AI tech booms that the US enjoyed, plus political turmoil in Germany and France, have further compounded economic weakness in the Eurozone, with equity returns of only 8.1%.

Asia & Emerging Equities

China also had a weak start to the year amidst falling property prices and low consumer confidence. This was counteracted by September policy updates which saw a rebound which jump-started their economy and ended the year on 19.8%. Japan also ended the year with a strong 20.5% amidst a positive wave about the end of deflation, a weak yen and ongoing corporate reforms.

The key question is whether the Chinese market rebound is sustainable and whether the demand for commodities remains robust (a big part of emerging market exports). Overall emerging market equities remained disappointing but are worth watching to see how they react to the ongoing recovery in more developed markets.

Fixed Interest Markets

Falling inflation and continued cutting of central bank interest rates perhaps reflected a year of (attempts) to return to normal. The ECB reduced rates from 4.25% to 3.15% and the Fed from 5.5% to 4.5%, while the Bank of England remains in a tricky position with the potential impact on employment after Labour’s budget in October.

The drop in inflation and subsequent rate cuts also showed that markets were expecting these changes. Yields showed surprising resilient to even large 0.50% rate cuts by the Fed, supporting the idea that investors have already priced in the expected changes.

This has led to attractive rates in government bonds, with US treasury notes yields nearly at 4%. These yields could become increasingly promising to investors as interest rates continue to fall. For the majority of 2024 though, the central banks reluctance to cut rates has led to a dampened corporate bond market. After all, why look to corporate bonds when you could secure a 5% interest rate on a money market fund? While yields steadily rose in Q4, the road ahead is still uncertain and rate cuts have already started to slow.

Concerns over inflation pressure as a result from a Trump’s unpredictable policy decisions have been seen as a potential for higher yields as central banks will not be willing to cut rates as aggressively going forward, turning to a “wait and see” position in response.